Today was a modest reset, not a regime shift. The S&P 500 closed at 7,108 and the Nasdaq at 24,439—the first red day since Monday, pulling back from Wednesday’s records. The tape made clear why: a concentrated software rout led by ServiceNow’s worst day on record, punctuated by IBM, a second Tesla leg lower, and the first genuinely uncomfortable PMI print of the year. This reads as sector-specific stress layered on top of live geopolitics, not the start of a broader correction. My framing remains constructive but hedged. Intel’s after-hours blowout—with Data Center and AI revenue up 22% year-over-year and a clean Q2 raise—validates that the earnings-led bull is alive, but highly selective. The market is willing to pay up for monetization evidence when a company actually delivers it.

The bigger message sits in the pattern. Roughly 81% of S&P 500 reporters are beating this quarter, yet names that beat without raising are being sold aggressively. ServiceNow beat and faded on explicit Iran-linked subscription headwinds; IBM and Tesla did the same on weak outlooks or massive capex raises. This is a “beat-and-fade” regime. The market is no longer accepting “good quarter, same outlook” to chase prices to records; it demands forward confirmation.

Looking to the Mag 4 next Tuesday, the bar remains unchanged: monetization is the test. We know Alphabet’s $175-$185B capex figure, but Cloud growth needs to clear 50%. Microsoft needs Azure constant-currency in the high 30s. Amazon needs AWS above 20%. Meta needs revenue growth to hold 32%. If they deliver, the software rout stays quarantined. If two or more miss on the forward outlook, the April rally will be severely tested. I want monetization evidence, and I am expressing that view through defined-risk options rather than outright directional bets.

On the macro side, stagflation is now in the tape. PMIs flagged manufacturing input costs at a 10-month high against slowing services, arriving exactly as Brent settles near $104 for its sixth straight session. With President Trump publicly ordering the Navy to destroy Iranian mine-laying vessels and declaring Hormuz “sealed up tight,” oil pass-through risk is materializing. Wednesday’s FOMC decision is the first real test of whether Chair Powell leans against the softer services read or holds the line against hotter input costs.

My Playbook: I am keeping the energy book on as an explicit hedge. I’m maintaining small-cap positioning at cheap 16x forward multiples with 17% consensus growth, leaning into semis over software after Intel, and running defined-risk options through Mag 4 and the FOMC. This tape still rewards staying engaged—it just demands doing it with hedges.

💰 The Income Generators (High Probability, Cash Flow)

MPC: Bullish Put Spread fading a short-term dip on a top-tier refiner acting as a geopolitical hedge.

IWM: Bullish Put Spread capitalizing on a regime shift toward broader small-cap market participation.

🚀 The Growth Seekers (Higher Risk, Max Reward)

(No trades in this category today)

🛡️ The Portfolio Protectors (Hedges & Bearish Bets)

BMY: Bearish Long Put Spread hedging against weak pharmaceutical flow, negative revisions, and a tough earnings setup.

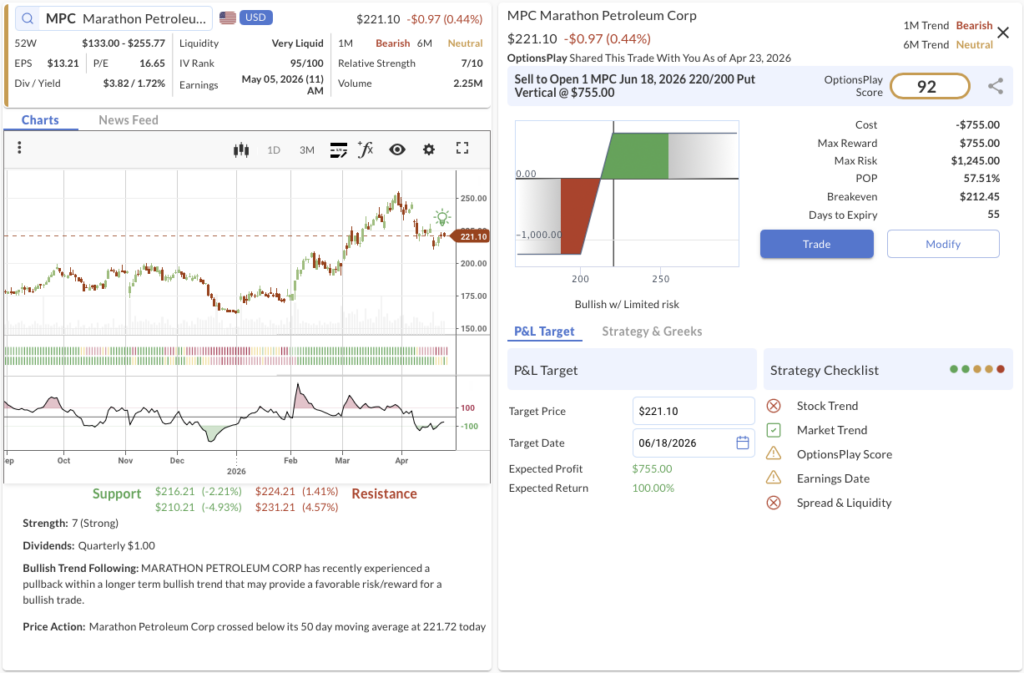

1. MPC ($221.10) – Hedging with the Refiners

We’re betting on: If oil remains elevated above $100 and domestic refiners continue to benefit from geopolitical risk premiums, MPC will bounce from its short-term pullback and hold above our $220 strike through June.

The Trade: Sell to Open the MPC Jun 18, 2026 220/200 Put Vertical @ $7.55 Credit.

🟢 BUY TO OPEN Jun 18, 2026 200 Put @ $5.00

🔴 SELL TO OPEN Jun 18, 2026 220 Put @ $12.55

Trade Metrics: POP: 57.52% | Collect $755.00 per contract vs. a Max Risk of $1,245.00 (1.6:1).

The Setup: Highlighted on our Iran Watchlist and Flow Dashboard, Marathon Petroleum serves as a critical structural hedge against the ongoing Hormuz disruptions. While the stock crossed below its 50-day moving average today, this short-term CCI pullback within a longer-term bullish structure provides a highly favorable risk/reward entry to sell premium on a defensively positioned energy leader.

Management:

⚠️ Warning: Earnings is scheduled for May 05, which may require active management.

Stop Loss: Buy back the spread at $15.10 (100% of credit received).

Take Profit: Buy back the spread at $3.78 (50% of max gain).

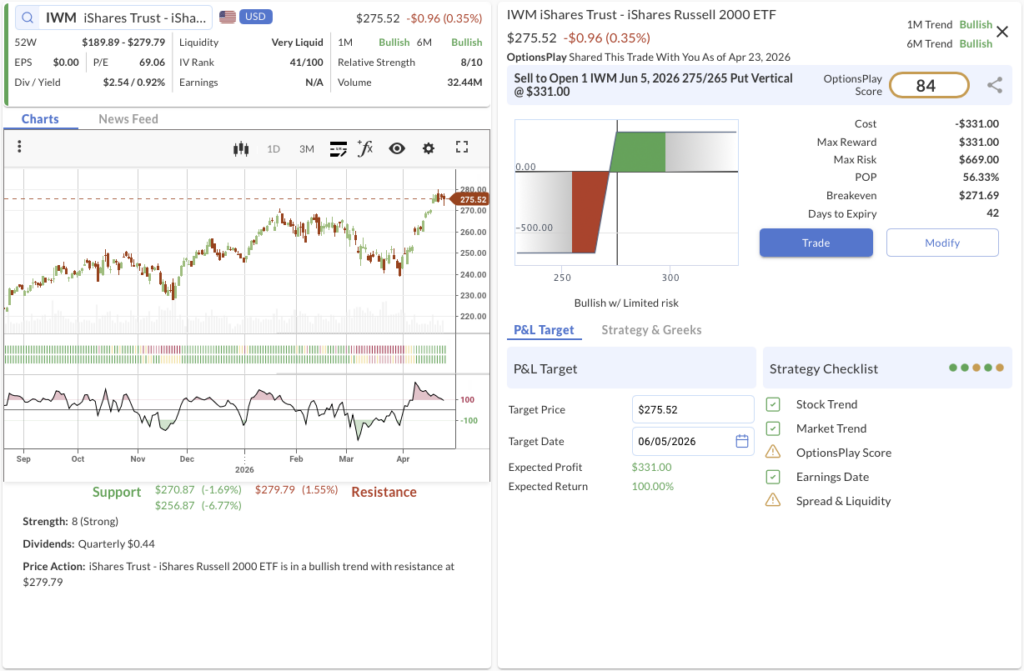

2. IWM ($275.52) – The Broadening Rotation

We’re betting on: If capital continues rotating out of concentrated tech and into under-owned domestic equities, small-cap breadth will expand, keeping IWM safely above our $275 strike.

The Trade: Sell to Open the IWM Jun 5, 2026 275/265 Put Vertical @ $3.31 Credit.

🟢 BUY TO OPEN Jun 05, 2026 265 Put @ $4.96

🔴 SELL TO OPEN Jun 05, 2026 275 Put @ $8.27

Trade Metrics: POP: 56.34% | Collect $331.00 per contract vs. a Max Risk of $669.00 (2.0:1).

The Setup: Small-cap breadth is building, marking an early regime shift from narrow mega-cap leadership to broader market participation. With domestic exposure, easing financial conditions, and an attractive 16x forward multiple, IWM is perfectly positioned to capture this rotation. Technically, the ETF is in a confirmed Bullish Trend (1M & 6M) with strong Relative Strength (8/10), making this a high-conviction trend-following setup.

Management:

Stop Loss: Buy back the spread at $6.62 (100% of credit received).

Take Profit: Buy back the spread at $1.66 (50% of max gain).

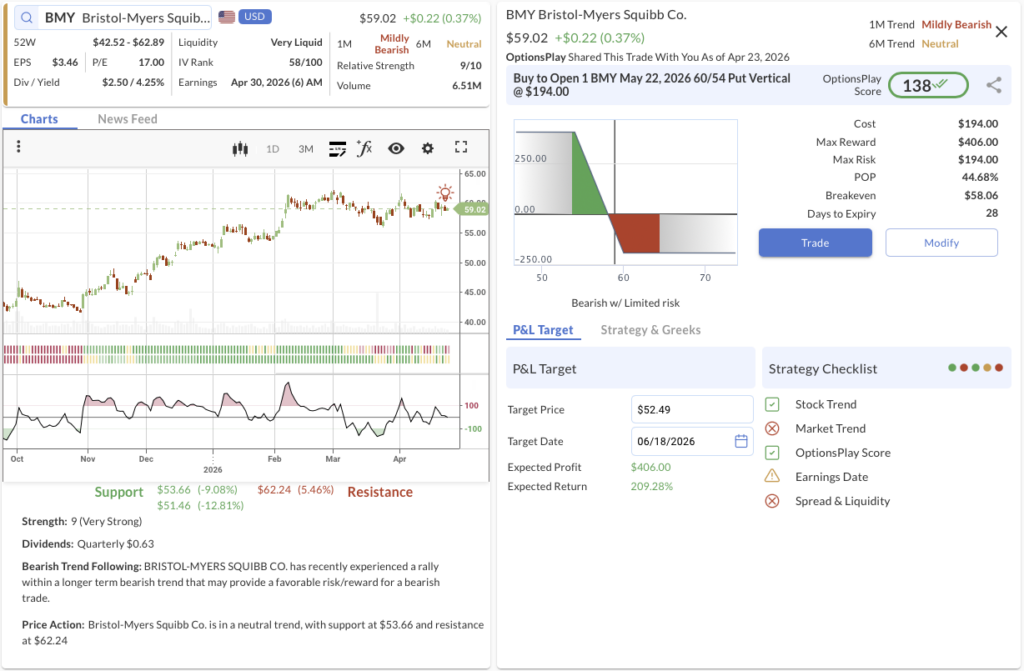

3. BMY ($59.02) – Fading the Pharma Flow

We’re betting on: If seasonal destocking, negative earnings revisions, and looming patent headwinds materialize during its earnings print, BMY will fail to hold support and drift lower, expanding the value of this debit spread.

The Trade: Buy to Open the BMY May 22, 2026 60/54 Put Vertical @ $1.94 Debit.

🔴 SELL TO OPEN May 22, 2026 54 Put @ $0.61

🟢 BUY TO OPEN May 22, 2026 60 Put @ $2.55

Trade Metrics: POP: 44.67% | Pay $194.00 per contract vs. a Max Reward of $406.00 (2.1:1).

The Setup: Bristol Myers Squibb heads into its April 30 earnings with a fundamentally weak setup. EPS is expected down roughly 19% year-over-year, and analyst sentiment is drifting lower. Our Flow Playbook specifically flags to “Avoid Pharma” right now, and the stock recently triggered a bearish trend-following alert. Because options volatility skew is unfavorable for a short call spread, utilizing a defined-risk long put vertical is the optimal way to play the downside.

Management:

⚠️ Warning: Earnings is scheduled for Apr 30, which may require active management.

Stop Loss: Sell the spread at $0.97 (50% loss on premium).

Take Profit: Sell the spread at $3.40 (75% gain on premium).

Share this on