Oil Was the Dominant Driver, Not Equities: WTI briefly broke below $70 intraday for the first time since March 2 and Brent settled down 4.3% at $73.74 as Hormuz tanker traffic kept climbing after the June 17 US-Iran MOU and the renewed Israel/Hezbollah ceasefire. As normalized throughput bleeds off the war-risk premium, the tape moved mechanically: energy was the worst sector, the 10-year yield collapsed 11 bps to 4.39% as inflation breakevens compressed, the VIX fell another 4.4% to 18.63, and the long-duration debasement hedges (gold -3.61% to $3,999.80, bitcoin -1.9%) all sold off in unison.

Equity Dispersion Was the Real Story: Headline indices were quiet (S&P -0.10%, Nasdaq -0.43%, Dow +0.35%, Russell +0.37%), but the rotation underneath was violent. The Dow’s outperformance came from defensive, value-tilted names insulated from both the energy unwind and the semi de-risking, while the Nasdaq’s weakness was almost entirely a chip story as traders cut exposure ahead of Micron’s after-hours print. Real estate and rate-sensitive groups got a bid on the duration rally, and small-caps eked out a gain on the combination of lower yields and cheaper input costs.

Micron Blew the Lid Off the AI-Memory Narrative: MU reported Q3 EPS of $25.11 versus $20.39 consensus and revenue of $41.5B versus $35.1B, a roughly $6.4B beat, with adjusted gross margin of 84.9%, a new $0.15 quarterly dividend, and Q4 revenue guided to $49 to $51B versus the $43.2B Street midpoint. The stock jumped more than 6% after hours and pulled the broader chip complex higher in extended trade, setting up Thursday’s open as a referendum on whether the HBM and AI-memory super-cycle thesis is still intact.

Single-Stock Moves and the Fed Backdrop: IBM extended gains after Tuesday’s JPMorgan upgrade to overweight, Qualcomm stayed under pressure on reported talks to acquire AI software firm Modular, and Oracle remained heavy after disclosing 21,000 job cuts. Wednesday’s bond rally was the energy and breakeven channel doing the work the Warsh Fed cannot, with fed funds futures still implying no cuts before year-end ahead of Friday’s May PCE print.

💰 The Income Generators (High Probability, Cash Flow)

RCL: Sell a put vertical to press a winning cruise position breaking out above $300.

🚀 The Growth Seekers (Higher Risk, Max Reward)

SPG: Long call vertical adding to a winning mall-REIT position at new 52-week highs, targeting $250.

🛡️ The Portfolio Protectors (Hedges & Bearish Bets)

(No trades in this category today)

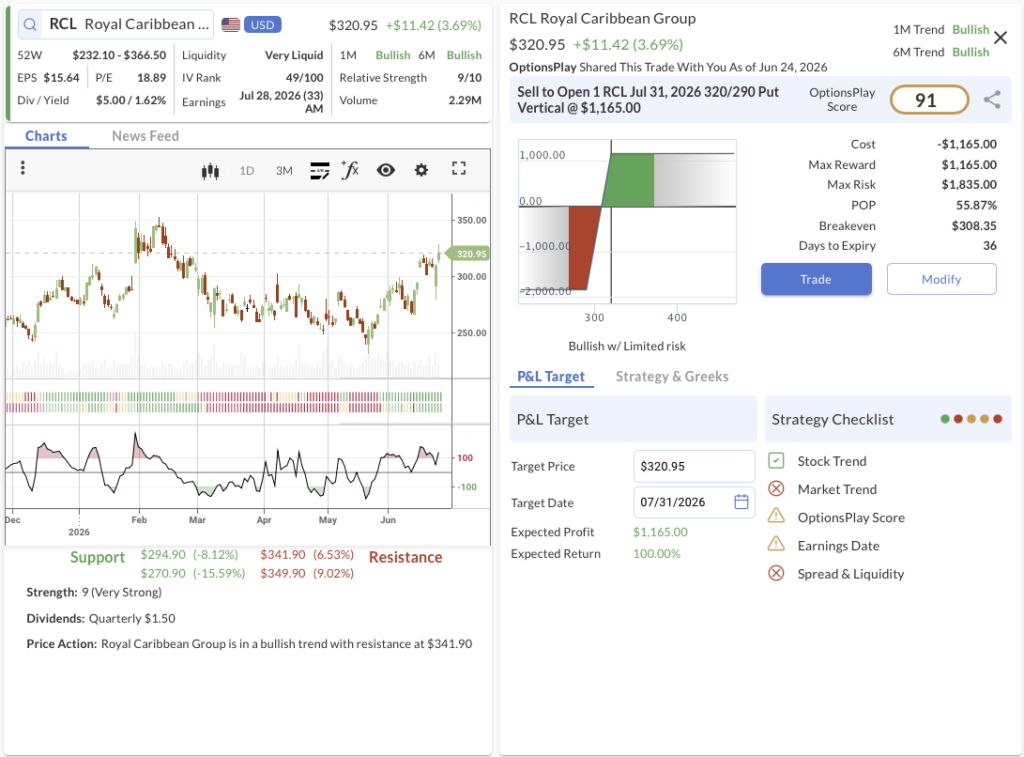

1. RCL ($320.95): Pressing a Cruise Winner Through $300

We’re betting on: Royal Caribbean’s record booking demand as travel keeps outperforming, pressing a winner already up about 19% on its breakout above $300 and upgrade to our building-outperformance list, and for RCL to stay above $320 by expiration to capture the full credit.

The Trade: Sell to Open the RCL Jul 31, 2026 320/290 Put Vertical @ $11.65 Credit.

🔴 SELL TO OPEN Jul 31, 2026 320 Put @ $20.35

🟢 BUY TO OPEN Jul 31, 2026 290 Put @ $8.70

Trade Metrics: POP: 55.88% | Collect $1,165 per contract vs. a Max Risk of $1,835 (1.58:1).

The Setup: This is the press-the-winner discipline: our June 16 RCL position, the 310/350 call vertical, is up about 19%, and RCL’s breakout above $300 with an upgrade to our building-outperformance list is the signal to add. The stock scores 8/10 on relative strength with both its 1M and 6M trends bullish as travel and cruise demand keep outperforming. Rather than chase with another debit, we sell the 320/290 put vertical to collect $1,165 and define risk below the $308.35 breakeven and the $294.90 support. With 37 days to expiry and a 55.88% probability of profit, time decay works in our favor as long as RCL holds above $320.

Management:

⚠️ Warning: Earnings are scheduled for July 28, 2026, potentially requiring active monitoring around the event.

Stop Loss: Buy back the spread at $23.30 (100% loss of credit received).

Take Profit: Buy back the spread at $5.83 (50% of max gain).

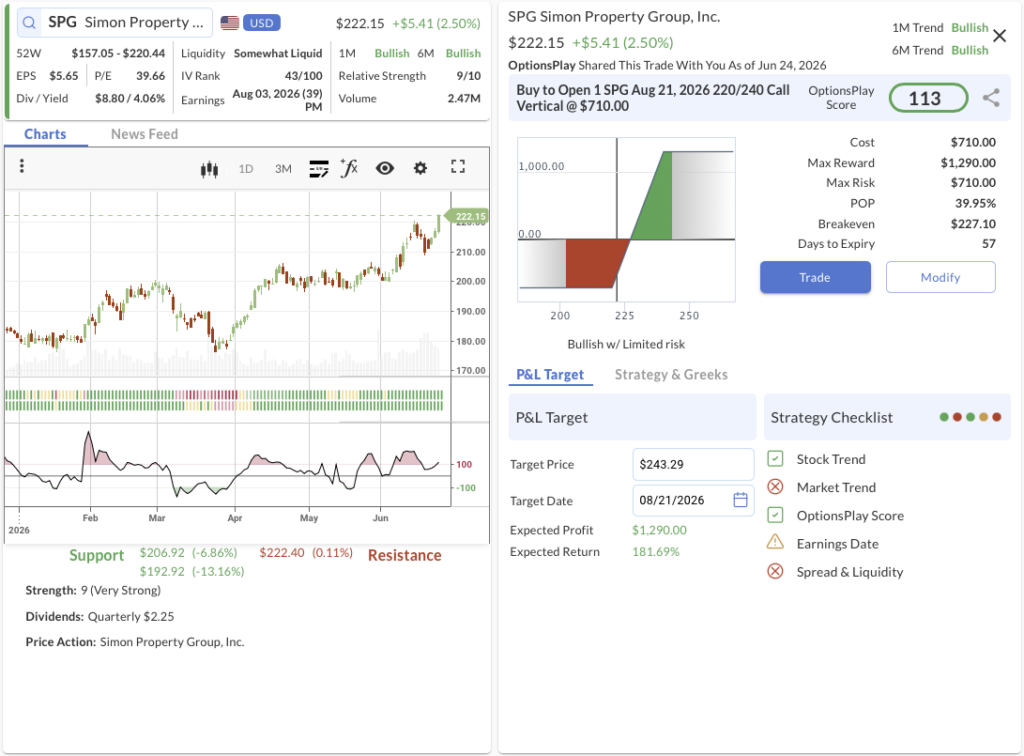

2. SPG ($222.15): Pressing a REIT Winner to New Highs

We’re betting on: Simon Property’s best-in-class mall REIT leadership as real estate outperforms, pressing a winner already up 66% on its breakout to new 52-week highs, and for SPG to close above $240 by expiration to capture the full spread.

The Trade: Buy to Open the SPG Aug 21, 2026 220/240 Call Vertical @ $7.10 Debit.

🟢 BUY TO OPEN Aug 21, 2026 220 Call @ $9.45

🔴 SELL TO OPEN Aug 21, 2026 240 Call @ $2.35

Trade Metrics: POP: 39.97% | Pay $710 per contract vs. a Max Reward of $1,290 (1.82:1).

The Setup: This is the press-the-winner discipline: our June 10 SPG position, the 210/230 call vertical, is already up 66%, and SPG’s breakout to new 52-week highs with an upgrade to our building-outperformance list is the signal to add further upside. The stock scores 9/10 on relative strength with both its 1M and 6M trends bullish as real estate outperforms on the duration rally. The 220/240 call vertical captures the continuation toward the $250 target with defined risk, a breakeven at $227.10, and support at $207, with a close above $240 at expiration delivering the full reward.

Management:

⚠️ Warning: Earnings are scheduled for August 3, 2026, potentially requiring active monitoring around the event.

Stop Loss: Sell the spread at $3.55 (50% loss of premium).

Take Profit: Sell the spread at $12.43 (75% gain on premium).

Share this on