Mag7 Split-Screen, Apple’s Worst Day in a Year: Apple fell 6.13%, its worst single session in over a year, after announcing the first formal pass-through of memory and storage cost inflation to consumers, raising MacBook and iPad list prices by as much as 25% while holding the line on iPhone, Watch, and AirPods. CEO Tim Cook called the move unavoidable, saying the company had never seen a component price increase this much this quickly, and Microsoft followed with Xbox hardware price hikes (-3.23%). The rest of the cohort leaned negative, with Nvidia, Oracle, Amazon, Alphabet, and Microsoft all down more than 2%.

Qualcomm Reframes as AI Infrastructure: QCOM ran as high as +11% to $219 intraday before settling +5% near $207 after its Investor Day doubled the FY29 non-handset revenue target to $40B from $22B (over $15B data center, about $10B automotive, over $14B IoT). It also landed Meta as its first named hyperscale data-center CPU customer and announced a roughly $4B all-stock acquisition of AI software startup Modular, positioned against NVIDIA’s CUDA moat. The size of the move showed how under-positioned the buyside was for the shift from smartphone IP to AI infrastructure.

Micron Extends, Memory Super-Cycle Confirmed: MU continued higher after Wednesday’s blowout (revenue $41.456B vs $35.59B consensus, +346% year over year, a Q4 guide near $50B vs $42.9B, gross margin 84.9%, 16 long-term agreements, and HBM fully booked beyond 2027), the cleanest AI capex confirmation in months. The irony is sharp: the same memory shortage powering Micron is now squeezing Apple’s margins with no near-term hedge.

Rotation Under the Surface as Oil’s War Premium Clears: The Dow held with 9 of 10 top names advancing (Caterpillar +4.04%, Goldman +1.15%) and the Russell 2000 rose 1.23% against the Nasdaq’s -0.46%, the cleanest rotation reading in weeks, as industrials, financials, and health care led. WTI fell below $70 for a fourth straight session (range $69.65 to $73.17) as Hormuz tanker traffic recovered and Brent broke decisively below $95, keeping energy-driven inflation pass-through contained even as core PCE drifts higher and the Fed stays on hold (July no-change odds near 89%).

💰 The Income Generators (High Probability, Cash Flow)

ABT: Sell a put vertical to establish a starter position on a med-tech breakout above $90.

🚀 The Growth Seekers (Higher Risk, Max Reward)

MRK: Long call vertical adding upside to a winning Merck position breaking out above $125.

🛡️ The Portfolio Protectors (Hedges & Bearish Bets)

(No trades in this category today)

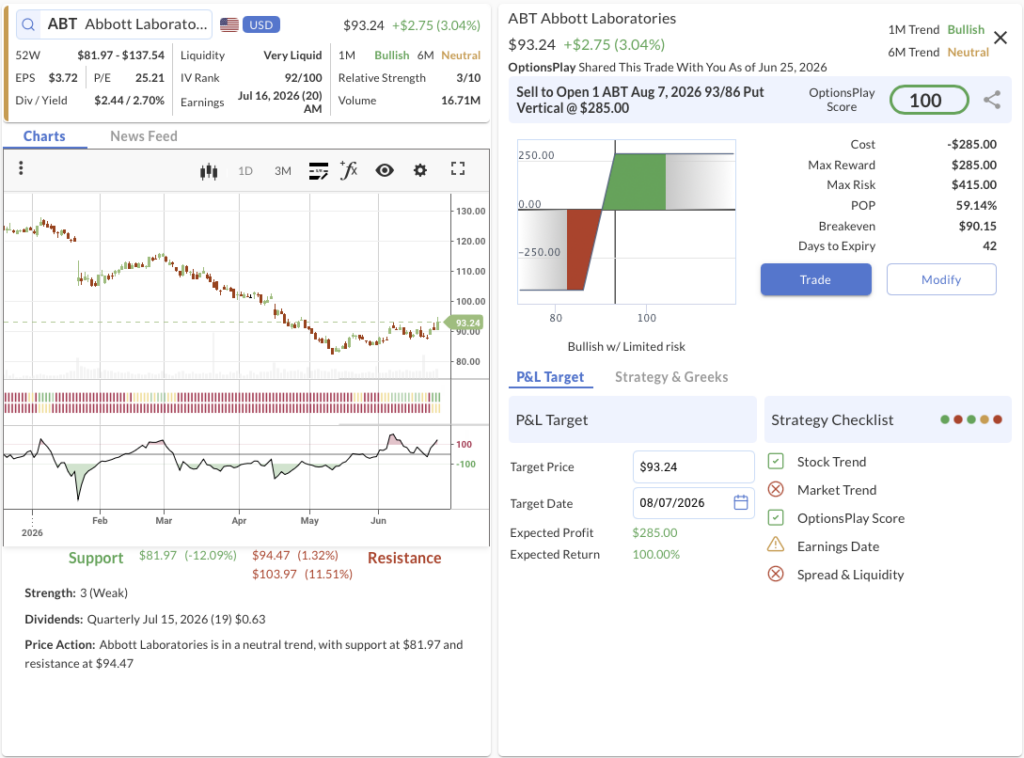

1. ABT ($93.24): Starter Position on the $90 Breakout

We’re betting on: Abbott’s diversified med-tech, diagnostics, and nutrition franchise stabilizing as it breaks out above $90, and for ABT to stay above $93 by expiration to capture the full credit.

The Trade: Sell to Open the ABT Aug 7, 2026 93/86 Put Vertical @ $2.85 Credit.

🔴 SELL TO OPEN Aug 7, 2026 93 Put @ $4.35

🟢 BUY TO OPEN Aug 7, 2026 86 Put @ $1.50

Trade Metrics: POP: 59.15% | Collect $285 per contract vs. a Max Risk of $415 (1.46:1).

The Setup: ABT recently broke out above its $90 level and triggered our early-breakout detector, warranting a starter position to see if it can move toward the $115 target. Relative strength is still weak at 3/10 with a neutral 6M trend, so this is an early-stage turnaround, which is why we establish exposure by selling defined-risk premium rather than buying the move outright. Selling the 93/86 put vertical collects $285 while defining risk below the $90.15 breakeven and just above the $81.97 support. With 43 days to expiry and a 59.15% probability of profit, time decay works in our favor as long as ABT holds above $93.

Management:

⚠️ Warning: Earnings are scheduled for July 16, 2026, potentially requiring active monitoring around the event.

Stop Loss: Buy back the spread at $5.70 (100% loss of credit received).

Take Profit: Buy back the spread at $1.43 (50% of max gain).

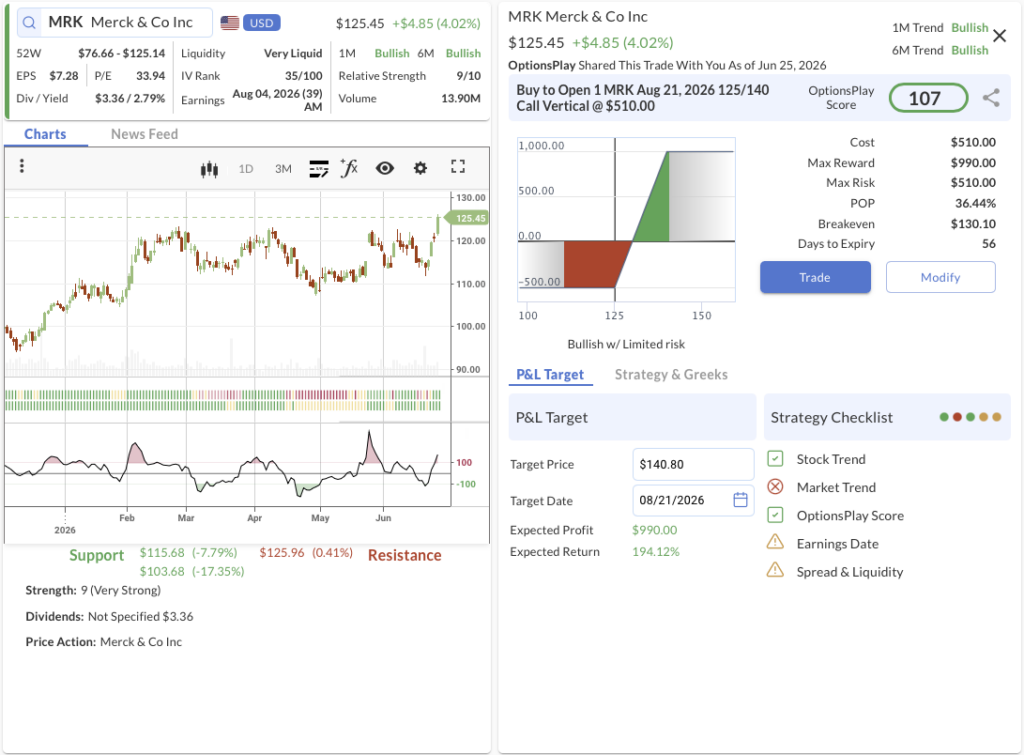

2. MRK ($125.45): Pressing a Pharma Winner Through $125

We’re betting on: Merck’s deep oncology and vaccine franchise re-rating on its breakout above $125, pressing a winner already up about 20%, and for MRK to close above $140 by expiration to capture the full spread.

The Trade: Buy to Open the MRK Aug 21, 2026 125/140 Call Vertical @ $5.10 Debit.

🟢 BUY TO OPEN Aug 21, 2026 125 Call @ $6.63

🔴 SELL TO OPEN Aug 21, 2026 140 Call @ $1.53

Trade Metrics: POP: 36.45% | Pay $510 per contract vs. a Max Reward of $990 (1.94:1).

The Setup: This is the press-the-winner discipline: our May 26 MRK position, the 122/115 put credit spread, is up about 20%, and MRK just broke out above $125 on strong volume with a fresh early-breakout scan, the signal to add directional upside. The stock scores 9/10 on relative strength with both its 1M and 6M trends bullish, backed by its durable Keytruda oncology engine and Gardasil vaccine franchise. The 125/140 call vertical captures the move toward the $140 target with defined risk, a breakeven at $130.10, and support at $115.68, with a close above $140 at expiration delivering the full reward.

Management:

⚠️ Warning: Earnings are scheduled for August 4, 2026, potentially requiring active monitoring around the event.

Stop Loss: Sell the spread at $2.55 (50% loss of premium).

Take Profit: Sell the spread at $8.93 (75% gain on premium).

Share this on